Session 08-02 - Annuities & Loan Amortization

Section 08: Financial Mathematics

Entry Quiz - 10 Minutes

Quick Review from Session 08-01

Test your understanding of Compound Interest

Find the 6th term of the geometric sequence: \(4, 12, 36, \ldots\)

Calculate the future value of 5,000 invested at 6% compounded quarterly for 5 years.

Find the effective annual rate for 8% compounded monthly.

How much should you invest today at 5% annual interest to have 15,000 in 8 years?

Learning Objectives

What You’ll Master Today

- Understand ordinary annuities and annuities due

- Calculate future value of regular payment streams

- Calculate present value of annuity payments

- Solve for payment amounts and number of payments

- Build loan amortization schedules

- Analyze interest vs. principal in loan payments

Part A: Introduction to Annuities

What is an Annuity?

An annuity is a series of equal payments made at regular intervals.

. . .

Examples:

- Monthly rent payments

- Salary deposits

- Loan repayments

- Retirement contributions

- Insurance premiums

. . .

The key: Equal payments at equal intervals

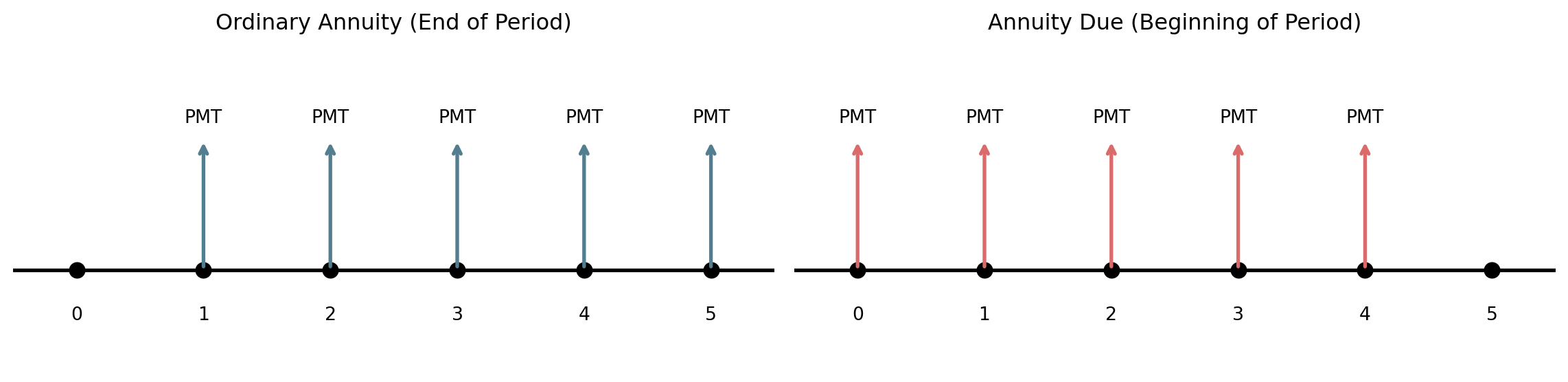

Types of Annuities

ImportantTwo Main Types

Ordinary Annuity (Nachschussig): Payments made at the end of each period

Annuity Due (Vorschussig): Payments made at the beginning of each period

. . .

Part B: Future Value of Annuities

Future Value of Ordinary Annuity

Question: If you save 500 per month at 6% annual interest, how much will you have in 10 years?

. . .

ImportantFuture Value Formula (Ordinary Annuity)

\[FV = PMT \cdot \frac{(1 + r)^n - 1}{r}\]

where:

- \(PMT\) = Payment per period

- \(r\) = Interest rate per period

- \(n\) = Total number of payments

FV Calculation Example

Given: 500/month, 6% annual (0.5% monthly), 10 years (120 months)

\[FV = 500 \cdot \frac{(1.005)^{120} - 1}{0.005}\]

. . .

\[FV = 500 \cdot \frac{1.8194 - 1}{0.005} = 500 \cdot \frac{0.8194}{0.005}\]

. . .

\[FV = 500 \cdot 163.88 = 81,939.67\]

. . .

Total deposits: \(500 \times 120 = 60,000\)

Interest earned: \(81,939.67 - 60,000 = 21,939.67\)

FV of Annuity Due

Payments at beginning of period earn one extra period of interest:

. . .

ImportantFuture Value Formula (Annuity Due)

\[FV_{\text{due}} = PMT \cdot \frac{(1 + r)^n - 1}{r} \cdot (1 + r)\]

Or simply: \[FV_{\text{due}} = FV_{\text{ordinary}} \cdot (1 + r)\]

. . .

Same example as annuity due: \[FV = 81,939.67 \times 1.005 = 82,349.36\]

Part C: Present Value of Annuities

Present Value of Ordinary Annuity

Question: How much is a stream of future payments worth today?

. . .

ImportantPresent Value Formula (Ordinary Annuity)

\[PV = PMT \cdot \frac{1 - (1 + r)^{-n}}{r}\]

. . .

Example: What is the present value of receiving 1,000/month for 5 years at 8% annual?

\[PV = 1000 \cdot \frac{1 - (1.00667)^{-60}}{0.00667} = 1000 \cdot 49.32 = 49,318.43\]

PV of Annuity Due

ImportantPresent Value Formula (Annuity Due)

\[PV_{\text{due}} = PMT \cdot \frac{1 - (1 + r)^{-n}}{r} \cdot (1 + r)\]

Or simply: \[PV_{\text{due}} = PV_{\text{ordinary}} \cdot (1 + r)\]

. . .

Same example as annuity due: \[PV = 49,318.43 \times 1.00667 = 49,647.32\]

Break - 10 Minutes

Part D: Solving for Unknowns

Finding the Payment Amount

Question: How much must you save monthly to have 100,000 in 15 years at 5%?

. . .

Rearrange the FV formula:

\[PMT = \frac{FV \cdot r}{(1 + r)^n - 1}\]

. . .

\[PMT = \frac{100000 \times 0.004167}{(1.004167)^{180} - 1} = \frac{416.67}{1.1137} = 374.26\]

. . .

You need to save 374.26 per month!

Finding Number of Payments

Question: How many months to pay off a 20,000 loan at 6% with 450/month payments?

. . .

From the PV formula, solve for \(n\):

\[n = -\frac{\ln(1 - \frac{PV \cdot r}{PMT})}{\ln(1 + r)}\]

. . .

\[n = -\frac{\ln(1 - \frac{20000 \times 0.005}{450})}{\ln(1.005)} = -\frac{\ln(0.7778)}{0.00499}\]

. . .

\[n = -\frac{-0.2513}{0.00499} = 50.4 \text{ months} \approx 51 \text{ payments}\]

Part E: Loan Amortization

What is Amortization?

Amortization = Paying off a loan through regular payments

. . .

Each payment consists of:

- Interest portion: Pays interest on remaining balance

- Principal portion: Reduces the loan balance

. . .

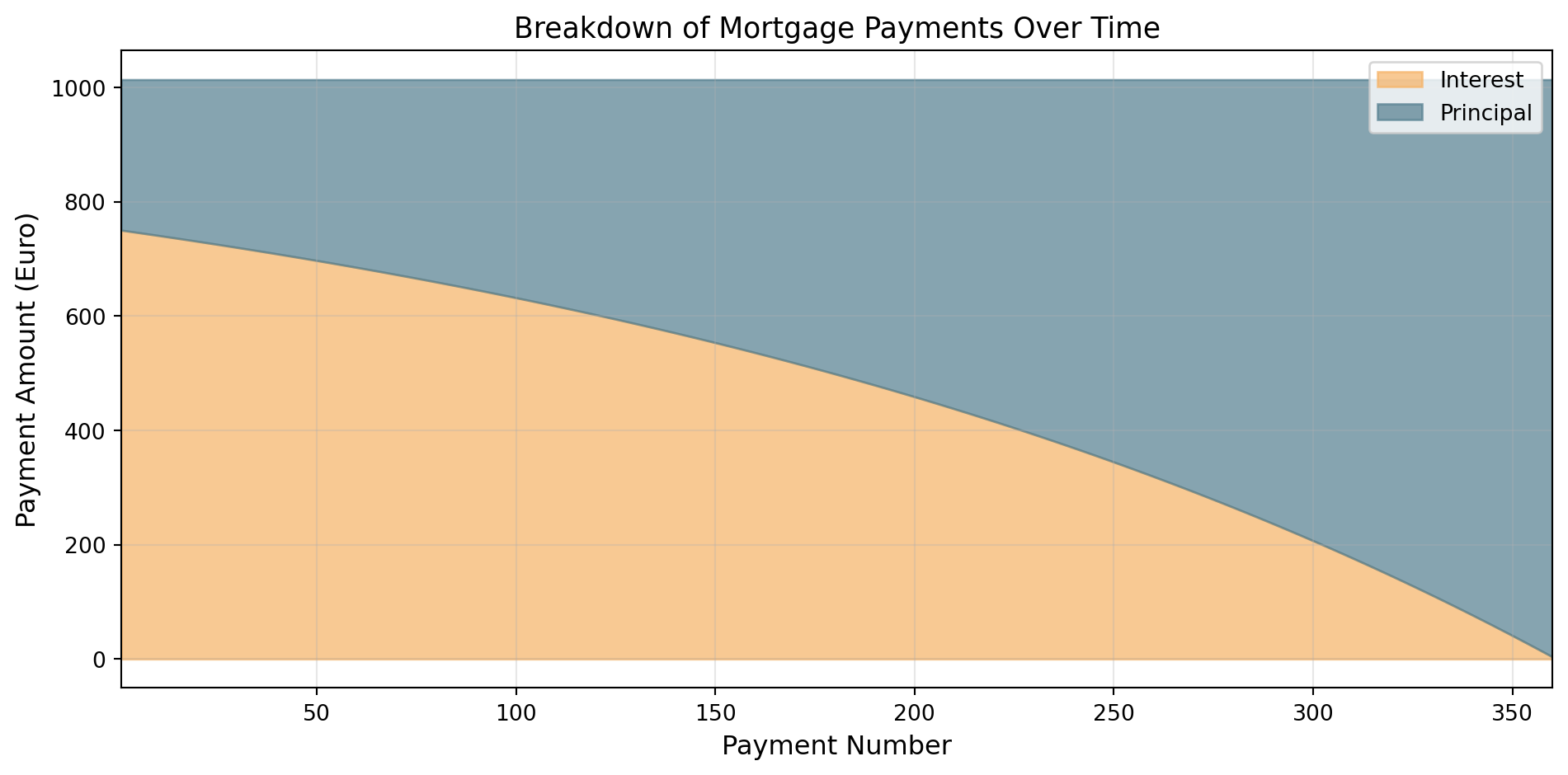

Key insight: Early payments are mostly interest, later payments are mostly principal!

Loan Payment Formula

ImportantMonthly Payment Formula

\[PMT = PV \cdot \frac{r}{1 - (1 + r)^{-n}}\]

where:

- \(PV\) = Loan amount (principal)

- \(r\) = Monthly interest rate

- \(n\) = Total number of payments

Payment Calculation Example

Loan: 200,000 at 4.5% annual for 30 years (mortgage)

\[r = 0.045/12 = 0.00375, \quad n = 360\]

. . .

\[PMT = 200000 \times \frac{0.00375}{1 - (1.00375)^{-360}}\]

. . .

\[PMT = 200000 \times \frac{0.00375}{1 - 0.2598} = 200000 \times \frac{0.00375}{0.7402}\]

. . .

\[PMT = 200000 \times 0.005067 = 1,013.37\]

Building an Amortization Schedule I

First few payments of the 200,000 loan:

| Payment | Payment | Interest | Principal | Balance |

|---|---|---|---|---|

| 0 | - | - | - | 200,000.00 |

| 1 | 1,013.37 | 750.00 | 263.37 | 199,736.63 |

| 2 | 1,013.37 | 749.01 | 264.36 | 199,472.27 |

| 3 | 1,013.37 | 748.02 | 265.35 | 199,206.92 |

| … | … | … | … | … |

Building an Amortization Schedule II

How it works:

- Interest: Balance \(\times\) rate = \(200,000 \times 0.00375 = 750\)

- Principal: Payment - Interest = \(1,013.37 - 750 = 263.37\)

- New Balance: Old Balance - Principal = \(200,000 - 263.37\)

Visualizing the Amortization

Outstanding Balance After k Payments

ImportantOutstanding Balance Formula

\[B_k = PV \cdot \frac{(1 + r)^n - (1 + r)^k}{(1 + r)^n - 1}\]

Or equivalently: \[B_k = PMT \cdot \frac{1 - (1 + r)^{-(n-k)}}{r}\]

. . .

Example: Balance after 10 years (120 payments) on the 200,000 mortgage

\[B_{120} = 1013.37 \times \frac{1 - (1.00375)^{-240}}{0.00375} = 1013.37 \times 158.59 = 160,706.24\]

Part F: Applications

Retirement Planning

Scenario: You want 500,000 at retirement in 30 years. Investment earns 7% annually.

How much must you invest monthly?

. . .

\[PMT = \frac{FV \cdot r}{(1 + r)^n - 1} = \frac{500000 \times 0.005833}{(1.005833)^{360} - 1}\]

. . .

\[PMT = \frac{2916.67}{7.878} = 370.16\]

. . .

Total invested: \(370.16 \times 360 = 133,257.60\)

Interest earned: \(500,000 - 133,257.60 = 366,742.40\) (more than 2.5x your contributions!)

Lease vs. Buy Decision

Should a company lease or buy equipment?

Buy: 50,000 now

Lease: 1,200/month for 4 years, then return

. . .

At 6% annual rate, PV of lease payments:

\[PV = 1200 \times \frac{1 - (1.005)^{-48}}{0.005} = 1200 \times 42.58 = 51,096.08\]

. . .

Leasing costs 51,096 in present value terms - buying at 50,000 is cheaper (before considering resale value of owned equipment).

Guided Practice - 15 Minutes

Practice Problems

Work in pairs

Problem 1: Calculate the future value of saving 300/month for 20 years at 5% annual interest.

Problem 2: Find the monthly payment for a 25,000 car loan at 4.8% for 5 years.

Problem 3: Create the first 3 rows of an amortization schedule for a 10,000 loan at 6% annual for 2 years (monthly payments).

Problem 4: How much is a monthly pension of 2,000 for 25 years worth today at 4% annual interest?

Wrap-Up & Key Takeaways

Today’s Essential Formulas

ImportantAnnuity Formulas

Future Value: \(FV = PMT \cdot \frac{(1 + r)^n - 1}{r}\)

Present Value: \(PV = PMT \cdot \frac{1 - (1 + r)^{-n}}{r}\)

Payment: \(PMT = PV \cdot \frac{r}{1 - (1 + r)^{-n}}\)

For annuity due: Multiply by \((1 + r)\)

Key Takeaways

- Annuities are equal payments at regular intervals

- FV of annuity tells you what regular savings will become

- PV of annuity tells you what a payment stream is worth today

- Amortization shows how loans are paid off

- Early payments are mostly interest, later payments mostly principal

. . .

TipComing Next

Session 08-03: Cost Analysis & Pricing Decisions - minimum pricing for profitability!

Homework Assignment

Tasks 08-02

- Calculate future and present values of annuities

- Solve for payment amounts and number of payments

- Build complete amortization schedules

- Apply concepts to retirement and loan decisions

. . .

These calculations require careful attention to the interest rate per period!