Session 08-01 - Compound Interest & Geometric Sequences

Section 08: Financial Mathematics

Entry Quiz - 10 Minutes

Quick Review from Section 07

Test your understanding of Probability

In a survey, 60% of customers are satisfied, 40% are repeat buyers, and 30% are both. Find \(P(\text{Satisfied OR Repeat})\).

A medical test has sensitivity 95% and specificity 90%. If disease prevalence is 2%, find the PPV.

A coin is flipped 4 times. Find \(P(\text{exactly 2 heads})\).

Create a contingency table: 100 people surveyed, 55 own cars, 40 own bikes, 20 own both.

Welcome to Financial Mathematics!

New Section Overview

Section 08 covers essential financial topics:

- Session 08-01: Compound Interest & Geometric Sequences (today)

- Session 08-02: Annuities & Loan Amortization

- Session 08-03: Cost Analysis & Pricing Decisions

. . .

Cost analysis and pricing decisions are exam-critical topics!

Learning Objectives

What You’ll Master Today

- Understand geometric sequences and their formulas

- Calculate compound interest for different compounding periods

- Find effective annual rates for comparison

- Apply present value concepts to business decisions

- Use the Rule of 72 for quick estimates

Part A: Geometric Sequences

What is a Geometric Sequence?

A sequence where each term is multiplied by a constant ratio:

. . .

\[a_1, \, a_1 \cdot r, \, a_1 \cdot r^2, \, a_1 \cdot r^3, \, \ldots\]

. . .

ImportantKey Formulas

Explicit formula (nth term): \[a_n = a_1 \cdot r^{n-1}\]

Recursive formula: \[a_n = a_{n-1} \cdot r\]

Examples of Geometric Sequences

Common ratio determines behavior:

. . .

\(r = 2\): \(3, 6, 12, 24, 48, \ldots\) (growth)

\(r = \frac{1}{2}\): \(16, 8, 4, 2, 1, \ldots\) (decay)

\(r = -2\): \(1, -2, 4, -8, 16, \ldots\) (alternating)

. . .

- \(|r| > 1\): sequence grows (or alternates with growth)

- \(|r| < 1\): sequence decays toward zero

- \(r = 1\): constant sequence

Part B: Compound Interest

Simple vs. Compound Interest

Two ways to grow money:

. . .

Simple Interest: Interest earned only on principal \[A = P(1 + rt)\]

. . .

Compound Interest: Interest earned on principal AND accumulated interest \[A = P(1 + r)^t\]

. . .

Compound interest creates exponential growth - this is where geometric sequences appear!

The Compound Interest Formula

Annual Compounding

\[A = P(1 + r)^t\]

. . .

where:

- \(A\) = Final amount (future value)

- \(P\) = Principal (initial investment)

- \(r\) = Annual interest rate (as decimal)

- \(t\) = Time in years

. . .

Example: Invest 1,000 at 5% for 10 years, \(A = 1000(1.05)^{10}\)

Multiple Compounding Periods

What if interest compounds more frequently?

. . .

General Compound Interest Formula

\[A = P\left(1 + \frac{r}{n}\right)^{nt}\]

where \(n\) = number of compounding periods per year

. . .

| Compounding | n |

|---|---|

| Annual | 1 |

| Semi-annual | 2 |

| Quarterly | 4 |

| Monthly | 12 |

| Daily | 365 |

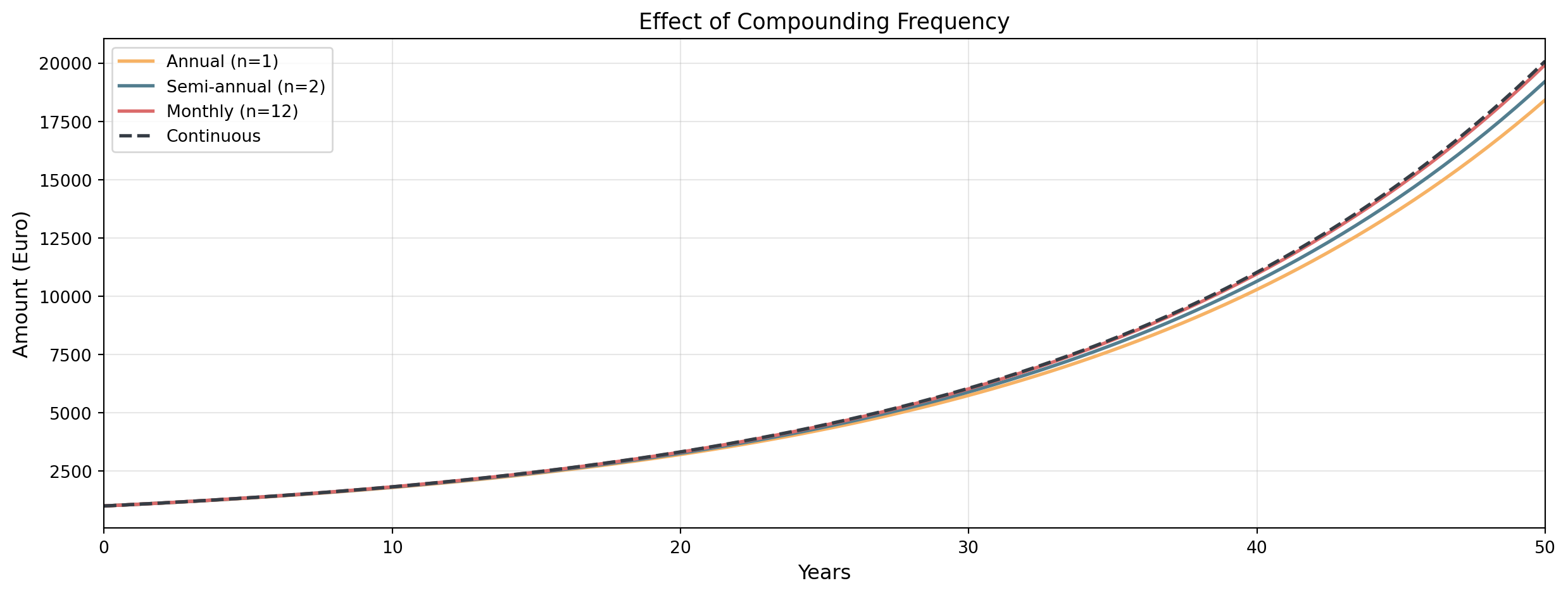

Compounding Comparison

1,000 invested at 6% for 50 years:

Continuous Compounding

As \(n \to \infty\), we get continuous compounding:

. . .

Continuous Compounding Formula

\[A = Pe^{rt}\]

where \(e \approx 2.71828\)

. . .

Derivation: \(\lim_{n \to \infty} \left(1 + \frac{r}{n}\right)^n = e^r\)

. . .

Example: 1,000 at 6% continuous for 5 years, \(A = 1000 \cdot e^{0.06 \times 5}\)

Break - 10 Minutes

Part C: Effective Annual Rate

Comparing Different Rates

Problem: Bank A offers 6% compounded monthly. Bank B offers 6.1% compounded annually. Which is better?

. . .

We need a common basis for comparison!

. . .

Effective Annual Rate (EAR)

\[r_{\text{eff}} = \left(1 + \frac{r}{n}\right)^n - 1\]

. . .

This gives the equivalent annual rate for any compounding frequency.

EAR Calculation Example

Bank A: 6% compounded monthly \[r_{\text{eff}} = \left(1 + \frac{0.06}{12}\right)^{12} - 1 = (1.005)^{12} - 1 = 0.0617 = 6.17\%\]

. . .

Bank B: 6.1% compounded annually \[r_{\text{eff}} = 6.1\%\]

. . .

Bank A is slightly better (6.17% > 6.10%)!

EAR for Continuous Compounding

For continuous compounding:

. . .

\[r_{\text{eff}} = e^r - 1\]

. . .

Example: 6% continuous compounding \[r_{\text{eff}} = e^{0.06} - 1 \approx 0.0618 = 6.18\%\]

Part D: Present Value

The Present Value Concept

Question: How much invest today to have 10,000 in 5 years at 6%?

. . .

We need to discount future values back to today.

. . .

Present Value Formula

\[PV = \frac{FV}{(1 + r)^t} = FV \cdot (1 + r)^{-t}\]

Present Value Example

Goal: 10,000 in 5 years at 6%

\[PV = \frac{10000}{(1.06)^5} = \frac{10000}{1.3382} = 7,472.58\]

. . .

You need to invest 7,472.58 today to have 10,000 in 5 years!

. . .

With monthly compounding: \[PV = \frac{10000}{(1 + 0.06/12)^{60}} = \frac{10000}{1.3489} = 7,413.72\]

Part E: Business Applications

Investment Growth Analysis

A company invests 50,000 in bonds paying 4.5% compounded quarterly.

- What is the value after 10 years?

- What is the effective annual rate?

- How long until the investment doubles?

Inflation Adjustment

Real Interest Rate (Fisher Equation)

\[r_{\text{real}} \approx r_{\text{nominal}} - r_{\text{inflation}}\]

. . .

Exact formula: \[1 + r_{\text{real}} = \frac{1 + r_{\text{nominal}}}{1 + r_{\text{inflation}}}\]

. . .

Example: 6% nominal return, 2% inflation \[r_{\text{real}} = \frac{1.06}{1.02} - 1 = 0.039 = 3.9\%\]

Guided Practice - 15 Minutes

Practice Problems

Work in pairs

Problem 1: Calculate the future value of 2,500 invested at 5.5% compounded monthly for 8 years.

Problem 2: Bank A offers 4.8% compounded daily. Bank B offers 4.9% compounded annually. Which bank offers a better return?

Problem 3: You need 25,000 in 6 years. How much must you invest today at 7% compounded quarterly?

Wrap-Up & Key Takeaways

Today’s Essential Concepts

- Geometric sequences have constant ratio: \(a_n = a_1 \cdot r^{n-1}\)

- Compound interest creates exponential growth

- More frequent compounding increases returns

- Effective annual rate allows fair comparison

- Present value discounts future amounts

- Rule of 72 estimates doubling time quickly

. . .

TipComing Next

Session 08-02: Annuities & Loan Amortization - regular payment streams!

Homework Assignment

Tasks 08-01

- Calculate geometric sequence terms and sums

- Compound interest with various compounding periods

- Compare investments using effective annual rates

- Present value calculations for financial planning

. . .

Practice with your calculator - these calculations appear frequently on exams!